Understanding Economic Growth and Development

Economic growth refers to the increase in an economy’s productive capacity and output over time, typically measured by the percentage change in gross domestic product (GDP). This metric indicates the total market value of all final goods and services produced within a country. As economies expand, they generate more wealth, which is crucial for improving living standards, reducing poverty, and expanding opportunities. However, it’s important to recognize that economic growth is primarily an accounting measure that reflects monetary transactions rather than a comprehensive gauge of societal progress. While GDP growth is often celebrated, it does not inherently translate into improved quality of life for all citizens. The focus on economic growth can sometimes overshadow essential aspects of development, such as education, health care, and social equity. Policymakers and economists must look beyond mere numbers to understand how growth affects the real-world experiences of individuals and communities. A deeper exploration of the relationship between economic growth and development reveals that while growth can create wealth, it does not automatically lead to equitable distribution or enhanced well-being for all members of society. This complexity underscores the need for a nuanced understanding of what constitutes true development in the modern world.

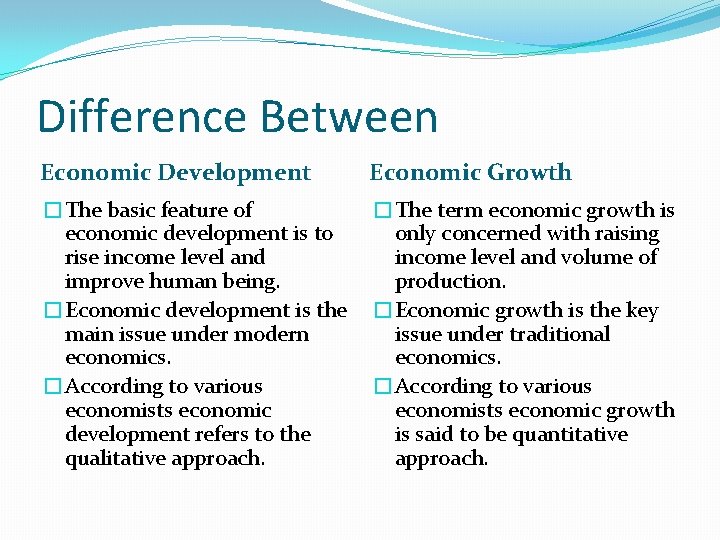

Differentiating Growth from Development

The distinction between economic growth and economic development is a critical one for understanding the broader implications of economic policies. Economic growth primarily focuses on quantitative measures, such as increases in GDP or productivity. In contrast, economic development encompasses qualitative improvements in individuals’ lives, aiming for a holistic enhancement of living standards. This includes advancements in education, health care, and social equity, which are vital for fostering a thriving society. Economic development seeks to remove constraints like poverty and discrimination, creating an environment where individuals can realize their full potential. This approach emphasizes the importance of social, political, and cultural factors in shaping economic outcomes. For policymakers, understanding this distinction is essential; they must create strategies that not only promote growth but also ensure that the benefits are widely shared. By prioritizing development, societies can work towards a future where economic success translates into improved quality of life for all citizens, not just a privileged few.

The Importance of Economic Growth

Economic growth is essential for raising national income and employment levels, leading to higher living standards. A growing economy creates jobs, increases disposable income, and enhances consumer spending, which in turn stimulates further growth. Additionally, economic growth plays a vital role in bolstering government finances through increased tax revenues. This financial boost enables governments to invest in infrastructure, education, and social services, further contributing to overall development. However, growth alone does not guarantee equitable wealth distribution or environmental sustainability. Rapid economic expansion can lead to income disparities and environmental degradation if not managed carefully. Therefore, it is crucial for policymakers to consider the broader implications of growth. A sustainable approach to economic growth involves not only maximizing output but also ensuring that the benefits are equitably distributed across different segments of society. By addressing issues of inequality and environmental impact, nations can work towards a more inclusive and sustainable model of growth that benefits everyone.

Types of Economic Growth

Economic growth can be categorized into various types, each with unique characteristics and implications for development. One significant type is the Boom and Bust Cycle, where economies experience rapid growth followed by downturns, as seen during events like the Great Recession. Understanding these cycles is crucial for policymakers to implement measures that can mitigate the negative impacts of downturns on society. Another type is Export-Led Growth, exemplified by countries like Japan and China, which leverage exports to boost their economies. This strategy often results in trade surpluses and can drive technological advancement, but it may also expose economies to global market fluctuations. On the other hand, Consumer-Led Growth is prevalent in the United States, where consumer spending drives economic expansion. While this model can create a vibrant economy, it can also lead to trade deficits and increased debt levels. Lastly, Commodity-Led Growth is seen in nations like Saudi Arabia, which depend heavily on natural resources for economic success. While this can yield significant revenues, it also poses risks during market fluctuations and can lead to over-reliance on volatile commodities. Understanding these various types of growth helps policymakers craft tailored strategies that address the unique challenges and opportunities each presents.

Factors Contributing to Economic Growth

Several key factors drive economic growth, each playing a crucial role in enhancing productivity and output. One of the most significant is the Labor Force. An increase in the workforce can enhance productivity, as more individuals contribute to the economy. This growth in labor supply is particularly important in developing countries, where demographic shifts can lead to increased economic potential. Capital Investment is another crucial factor. Investments in physical capital, such as machinery and infrastructure, improve efficiency and production capacity. Higher levels of investment can lead to technological advancements and innovation, further driving growth. Similarly, Technological Innovation is a vital contributor. Advances in technology can lead to significant productivity gains, allowing economies to produce more with less effort. Lastly, Human Capital plays a pivotal role in economic growth. Improving the skills and education of the labor force directly impacts economic performance. A well-educated workforce is more adaptable and innovative, driving progress across various sectors. By focusing on these key factors, governments and organizations can create conditions that foster sustainable economic growth.

Impediments to Economic Growth

While various factors can contribute to economic growth, several impediments can hinder progress. One significant challenge is Inadequate Infrastructure. Poor infrastructure limits productivity and increases costs, making it difficult for businesses to operate efficiently. Countries with inadequate roads, transportation systems, and utilities often struggle to attract investment and stimulate economic activity. Political Instability is another critical barrier. Uncertain political environments can discourage both domestic and foreign investment, leading to reduced economic activity. Investors often seek stable environments where their investments are protected, and political turmoil can erode confidence and lead to capital flight. Additionally, Poor Health and Education can severely limit workforce productivity. Low levels of health and education not only reduce individual potential but also strain public resources. Finally, Regulatory Barriers can stifle innovation and investment. Excessive regulations can create unnecessary hurdles for businesses, making it difficult for them to thrive. Addressing these impediments is essential for creating an environment conducive to sustained economic growth.

The Role of Government in Economic Growth

Governments play a critical role in fostering an environment conducive to economic growth. As noted by Adam Smith, the foundational elements of prosperity include “peace, easy taxes, and a tolerable administration of justice.” These principles highlight the importance of stable governance in promoting economic activity. Effective governance should focus on maintaining stability, minimizing excessive taxation, and ensuring fair legal frameworks that encourage investment. Moreover, governments must strike a balance between intervention and laissez-faire policies. While some level of regulation is necessary to protect consumers and the environment, excessive intervention can stifle innovation and slow growth. By creating a favorable business climate, governments can attract both domestic and foreign investment, which is essential for economic expansion. In addition to fostering a positive investment climate, governments also have a role in addressing social inequalities and ensuring that the benefits of growth are widely shared. By investing in education, health care, and infrastructure, governments can empower their populations and create a more equitable society. Ultimately, the role of government is multifaceted, requiring a careful balance of policies that promote growth while ensuring social and environmental sustainability.

Measuring Economic Growth

Economic growth is commonly measured through indicators like GDP and Gross National Product (GNP). These metrics provide insights into a country’s economic health and performance. However, while GDP is a valuable tool, it does not capture the full spectrum of societal well-being. For example, GDP growth might occur alongside rising inequality or environmental degradation, raising questions about the overall quality of life. Alternative measures are increasingly being explored to assess development comprehensively. Indices that consider environmental sustainability, social equity, and quality of life provide a more nuanced view of a country’s progress. For instance, the Human Development Index (HDI) incorporates health, education, and income indicators to provide a broader perspective on development. Policymakers are increasingly recognizing the limitations of traditional economic indicators. By embracing a more holistic approach to measuring growth, societies can ensure that economic policies prioritize the well-being of individuals and communities. This shift towards comprehensive measurement reflects a growing awareness of the interconnectedness of economic, social, and environmental factors in shaping sustainable development.

Conclusion: The Future of Economic Growth and Development

The relationship between economic growth and development is complex and multifaceted. While economic growth can serve as a means to achieve development goals, it is not sufficient on its own. Policymakers must focus on creating inclusive growth that benefits all segments of society. This involves addressing the constraints to development and prioritizing sustainable practices that promote long-term well-being. As we move forward, it is essential to recognize that the challenges of the 21st century—such as climate change, inequality, and technological disruption—require innovative and adaptive approaches to economic growth. By fostering an environment that promotes social equity, environmental sustainability, and economic opportunity, societies can create a prosperous future for individuals and communities alike. Emphasizing a balanced approach to growth and development will be crucial in navigating the complexities of a rapidly changing global landscape.

Sponsored Links